Consumer Bankruptcy filings continue to rise month over month leading many dealerships reporting a noticeable trend: customers are ready to buy shortly after filing for bankruptcy. These individuals are not the traditional “bad credit” shopper. Many are caught in unforeseen medical expenses or job loss. Many quickly find that they qualify for financing that fits their budget.

Consumer Bankruptcy filings continue to rise month over month leading many dealerships reporting a noticeable trend: customers are ready to buy shortly after filing for bankruptcy. These individuals are not the traditional “bad credit” shopper. Many are caught in unforeseen medical expenses or job loss. Many quickly find that they qualify for financing that fits their budget.

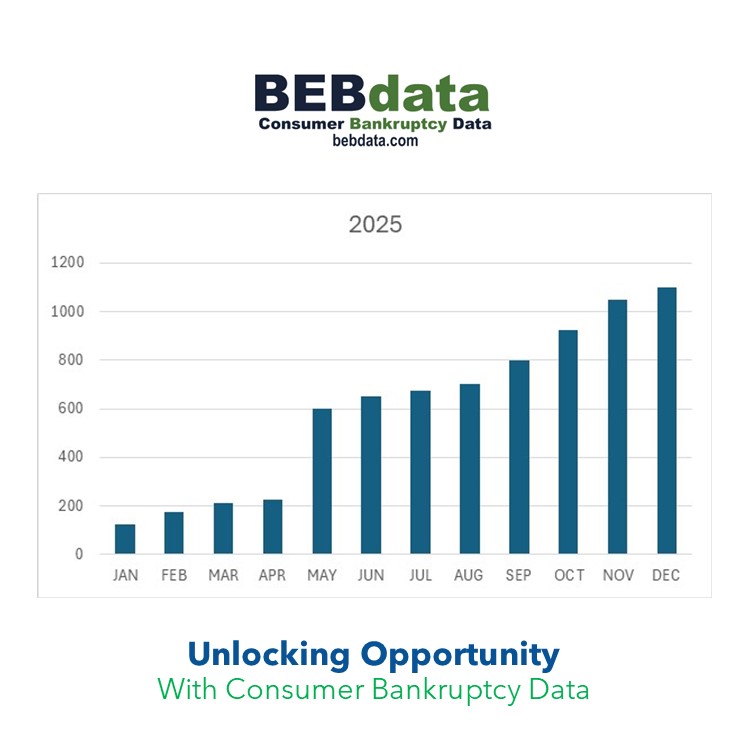

The increase in bankruptcy filings opens up new opportunities for dealerships to work with consumers who have been financially strained. Factors such as the return of student loan collections and the end of certain financial modification programs are expected to escalate filings further in the near future. This growing wave of bankruptcy leads has created an uptick in activity with these potential customers. Many lenders are willing to extend credit immediately following bankruptcy filings, presenting an opportunity for dealerships to nurture relationships with these potential buyers. Dealerships ready to embrace this segment of the market, are primed for growth in sales. Consumer bankruptcy is a bridge to new opportunities.

Translate