We made it! Have a safe and happy New Year.

We made it! Have a safe and happy New Year.

From all of us at BEBdata, we wish you and yours a very safe and happy Christmas Holiday.

From all of us at BEBdata, we wish you and yours a very safe and happy Christmas Holiday.

As always, thank you for your business and partnership.

The Passenger Car Market will reach 1598.21 billion USD by 2025. A Passenger car can be defined as a car designed for carrying only a few people. Passenger vehicles are the most common mode of transport and the number is increasing in developed as well as developing countries.

The Passenger Car Market will reach 1598.21 billion USD by 2025. A Passenger car can be defined as a car designed for carrying only a few people. Passenger vehicles are the most common mode of transport and the number is increasing in developed as well as developing countries.

92% of people buying cars today already research online. This year we saw a complete online car buying journey emerge including purchase and delivery. People want online car buying.

92% of people buying cars today already research online. This year we saw a complete online car buying journey emerge including purchase and delivery. People want online car buying.

Prior to the pandemic, only a few dealerships had online capabilities to execute a full online experience. While the purchase journey itself was happening online, the purchase remained offline. Since COVID-19, at-home test drives and vehicle delivery were tied as the number 1 alternative to visiting a car dealership for shoppers.

At a time when social restrictions related to the pandemic are impacting consumer behavior, developing strategies for how to meet consumer demand for online buying and at-home delivery can make a large impact: 18% of auto shoppers would buy a vehicle sooner if they could purchase the vehicle they wanted without going to a dealership.

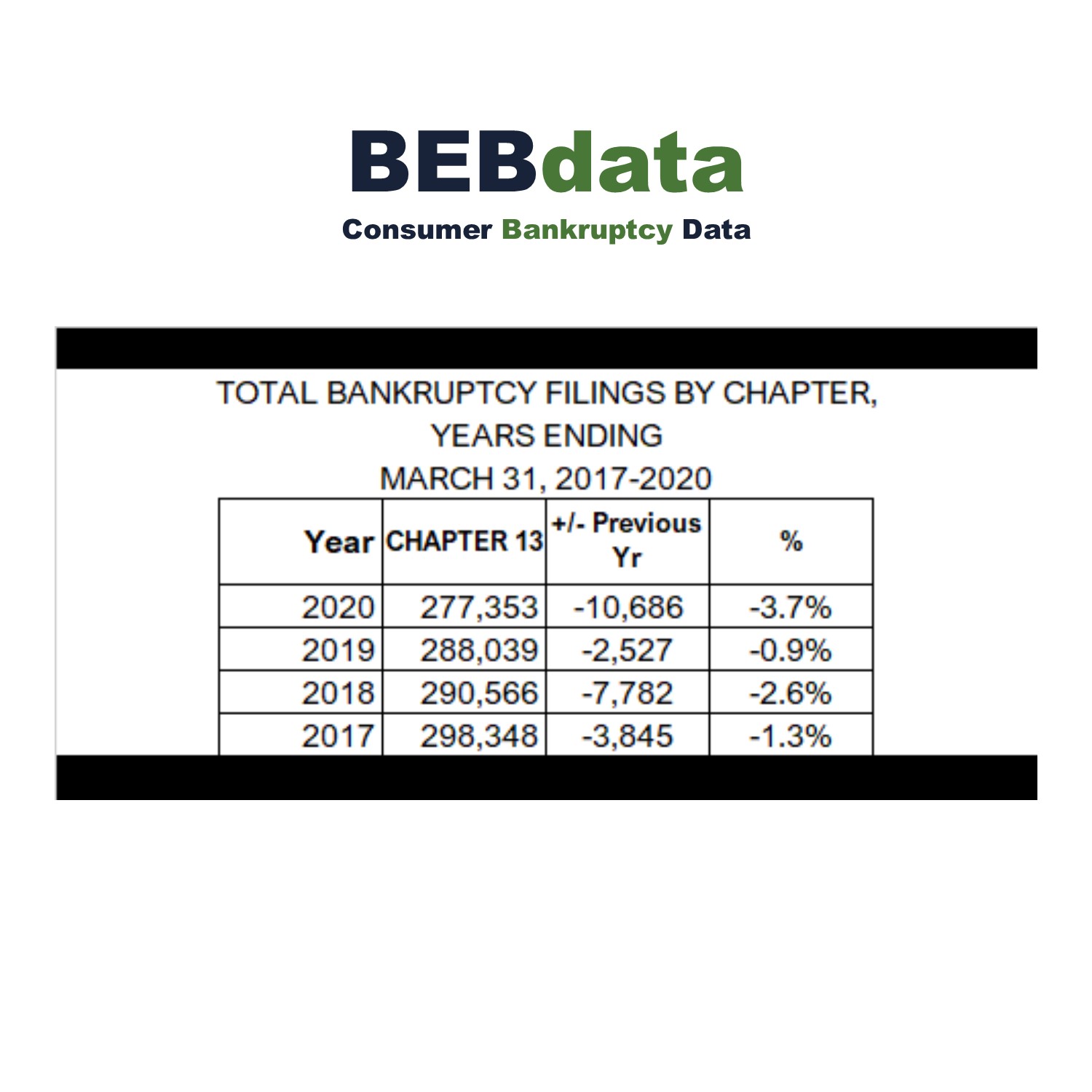

The chart above shows Chapter 13 filings for years ending March 31, 2017 – 2020.

The chart above shows Chapter 13 filings for years ending March 31, 2017 – 2020.

Wishing you a safe and happy Thanksgiving holiday.

Wishing you a safe and happy Thanksgiving holiday.

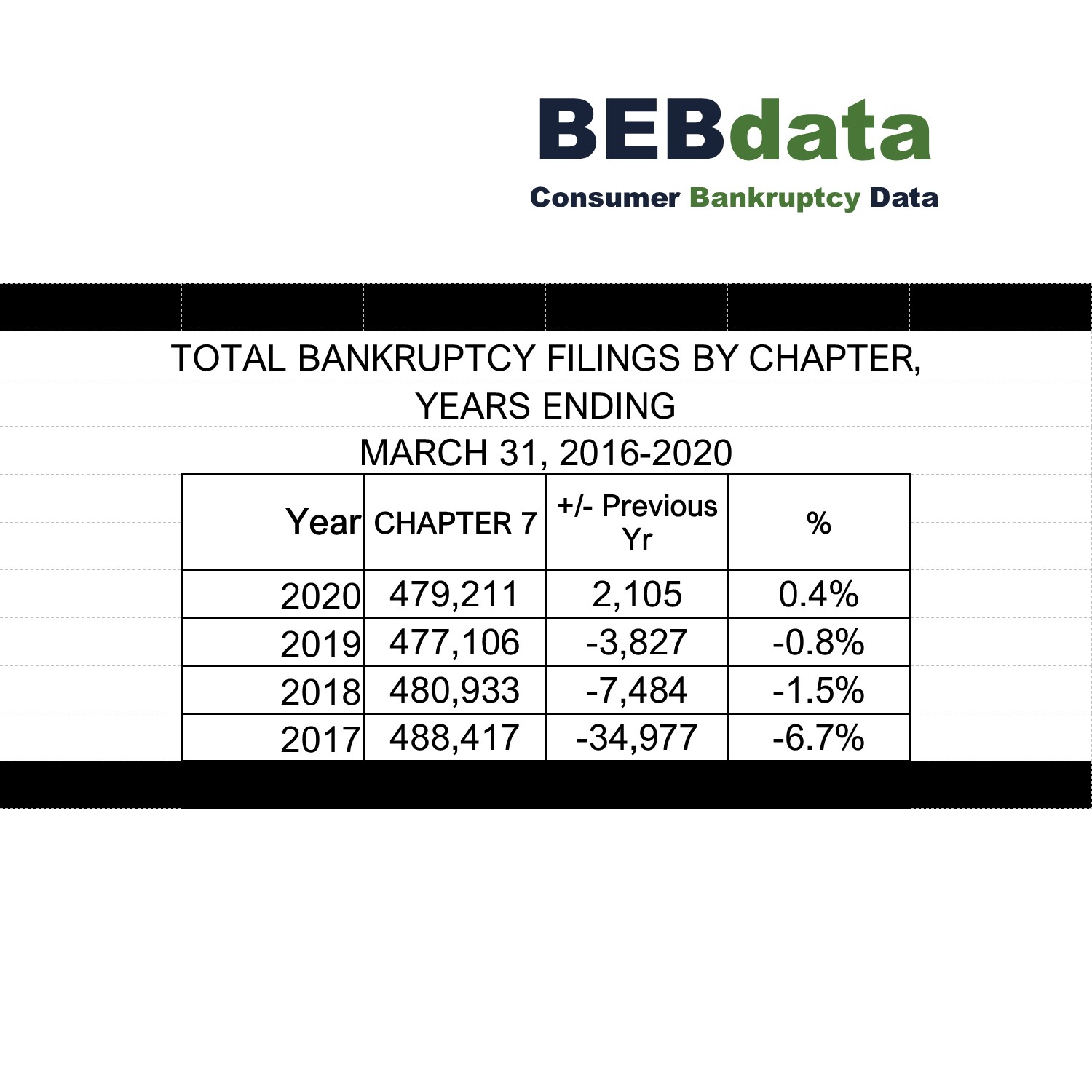

The above chart show total bankruptcy filing by Chapter 7 for years ending March 31st.

The above chart show total bankruptcy filing by Chapter 7 for years ending March 31st.

From all of us at BEBdata, Thank You to all Veterans. We appreciate your service.

Around 530,000 bankruptcy cases are filed every year due to inability to pay medical expenses.

Around 530,000 bankruptcy cases are filed every year due to inability to pay medical expenses.

54% of Americans with medical debt, have no other debt.

Wishing you a very safe and happy Halloween from all of us at BEBdata!