Marketers anticipate a period of adjustment in 2023 for used car sales. Affordability due to higher interest rates and inventory challenges point to an anticipated slight decrease in sales.

Marketers anticipate a period of adjustment in 2023 for used car sales. Affordability due to higher interest rates and inventory challenges point to an anticipated slight decrease in sales.

Marketers forecast 18.9 million in retail used car sales for 2023 and 35.6 million for overall used sales.

Used car sales were down in 2022, with the rolling 30-day retails sales 9% behind 2021. The average listing price also saw a 4% decrease to $27,077.

By end of 2022, the used market saw a double-digit drop in vehicles priced between $25,000 and $30,000 and a near 10% drop in vehicles between $20,000 and $25,000. There has been a steady growth in wholesale inventory over the past six months.

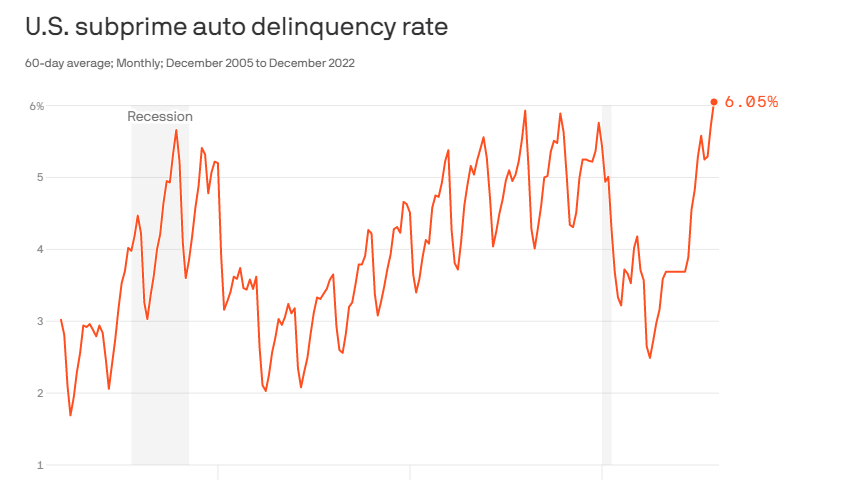

However, as prices retreat for used vehicles from record highs, affordability remains an issue, with high interest rates, 12%-13%. Rates are expected to climb, as the Federal Reserve tries to bring down inflation. The Fed in the past year has raised rates 425 basis points — the highest annual adjustment on record. The rising rates have dramatically impacted the subprime market. But the higher interest rates and costs have caused demand to slide throughout the industry.

The industry is trading a supply problem for a demand problem. With higher expenses comes lower demand.

Interest rates are not expected to decrease though hikes are expected to slow during the 3rd and 4th quarter.

Certified preowned vehicles (CPP) are expected to remain in short supply. Vehicles usually available for the CPO market were entering the rental car market at a higher rate throughout 2021 and 2022. CPO sales are expected to be around 2.2 million this year.

RESOURCE: National Independent Auto Dealers Association

The 2023 Used Car Market

Leave a reply