TransUnion forecasts serious credit card delinquencies to rise to 2.60% at the end of 2023 from 2.10% at the conclusion of 2022. Unsecured personal loan delinquency rates are expected to increase from 4.10% to 4.30% in the same timeframe. Serious auto loan delinquency rates are expected to modestly decline to 1.90% in 2023 from 1.95% in 2022.

TransUnion forecasts serious credit card delinquencies to rise to 2.60% at the end of 2023 from 2.10% at the conclusion of 2022. Unsecured personal loan delinquency rates are expected to increase from 4.10% to 4.30% in the same timeframe. Serious auto loan delinquency rates are expected to modestly decline to 1.90% in 2023 from 1.95% in 2022.

TransUnion’s forecasts are based on various economic assumptions, such as expected consumer spending, disposable personal income, home prices, inflation, interest rates, real GDP growth rates and unemployment rates, among other metrics. The forecasts could change if there are unanticipated shocks to the economy, such as if COVID-19 disrupts recovery efforts, home prices unexpectedly fall or inflation continues to remain elevated through the next year. Better-than-expected improvements in the economy, such as potential increases in GDP and disposable income, could also impact these forecasts.

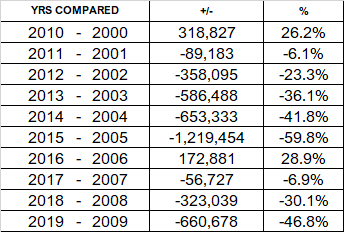

Serious CC Delinquencies Expected to Rise in 2023

Leave a reply